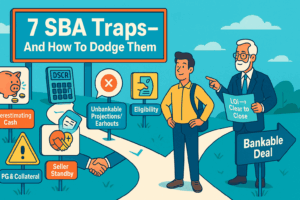

7 SBA Traps First-Time Buyers Miss

SBA financing is powerful—low down, long terms—but first-time buyers often hit avoidable pitfalls. Here’s what to watch for and how to dodge it.

-

Prequalification ≠ Approval: Treat prequalifications as directional only; plan around full approval and a clear-to-close status.

-

Underestimating Cash at Close: Build a comprehensive list of sources & uses early (including injection, SBA guarantee fee, bank/legal/QoE/appraisal/environmental, packaging, working capital, and first payroll).

-

DSCR That Won’t Survive: Use conservative recasts, include a market owner salary, stress-test rates; if DSCR < ~1.20x, adjust price/terms.

-

Unbankable Price/Structure: Projections/earnouts rarely fly; tie price to historical cash flow; use standby, subordinated seller notes or pre-close price adjustments.

-

Eligibility Landmines: Screen early for business type, franchise registry, citizenship/residency, affiliate size, and government-debt issues.

-

Seller Note Terms: If counting as equity, require full standby + subordination; otherwise model payments to protect DSCR.

-

PG/Collateral/Insurance Surprises: Confirm personal guarantees, spousal consents, collateral expectations (incl. home equity), and life insurance up front.

Pre-Offer Fit Test: ≥1.20x DSCR after buyer salary and all debt; price aligns with historical earnings; sources & uses covers all fees + working capital; any seller note is subordinated and on standby if counted as equity; no eligibility red flags; timeline reflects QoE/appraisal/environmental.

Quick Q&A

Q: How much down do I need?

A: Many SBA 7(a) deals land around 10% total injection (some mix of buyer cash and/or a fully-standby seller note), but specifics vary by lender and deal risk.

Q: Are earnouts allowed?

A: Typically, no for SBA—use standby seller notes or price adjustments before closing instead.

Q: Will lenders use projections?

A: Projections can inform risk, but approvals hinge on bankable historical cash flow and realistic normalization.

Q: What timeline should I expect?

A: Think 45–75+ days from signed LOI to close, depending on underwriting and third-party reports.

Have questions? Let’s talk..